The rescheduling of Donald Trump’s state visit to China for May 14-15 represents more than a logistical adjustment; it is a tactical recalibration necessitated by the collapse of the Middle East security architecture and the shifting marginal utility of a bifurcated trade policy. While the initial delay was attributed to Iranian regional destabilization, the new timeline suggests a strategic pivot toward a "Grand Bargain" framework. This framework seeks to trade American security guarantees in the Strait of Hormuz for structural concessions in Chinese industrial subsidies and intellectual property enforcement.

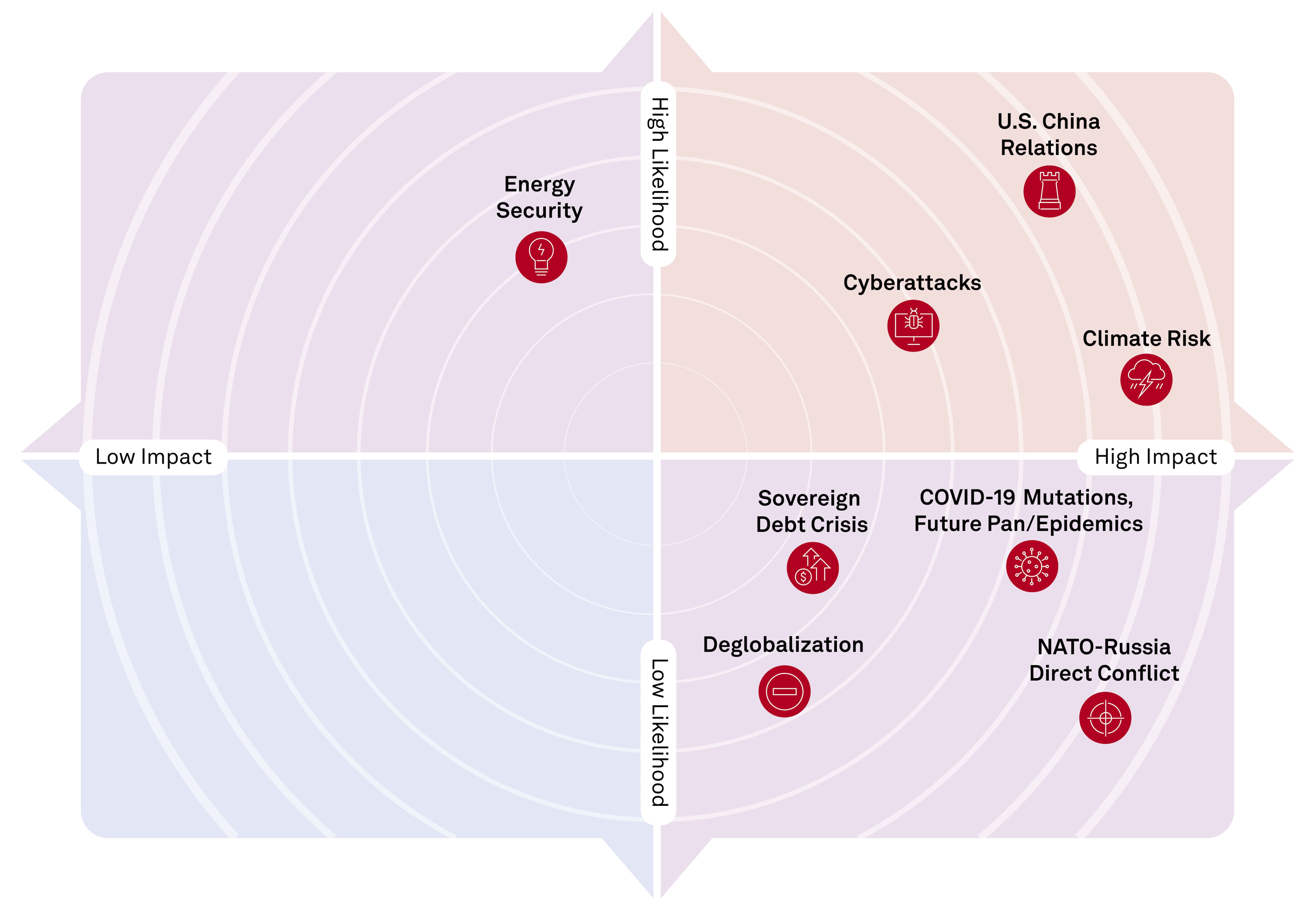

The delay served as a stress test for both economies. By analyzing the period between the original date and the new May 14 window, we identify three distinct friction points that will define the success or failure of the summit: the Energy Security Interdependency, the Semiconductor Sovereignty Gap, and the Currency Valuation Equilibrium.

The Energy Security Interdependency

China’s reliance on Iranian crude oil creates a persistent vulnerability in its energy supply chain. The U.S. executive branch uses this dependency as a lever. By delaying the China visit following Iranian-linked disruptions, the Trump administration signaled that Beijing’s access to global energy markets is contingent upon its cooperation in isolating Tehran.

The logic follows a specific cost-benefit function:

- Input: U.S. naval presence in the Persian Gulf ensures the flow of 20% of global oil.

- Variable: Chinese demand accounts for roughly 25% of that flow.

- Outcome: If China provides a backstop for the Iranian economy, the U.S. de-prioritizes the "Safe Passage" protocols, increasing the insurance premiums and freight costs for Chinese tankers.

The May 14 date is timed to coincide with the expiration of several temporary waivers regarding shipping sanctions. This forces President Xi to enter the summit not as an equal partner in a trade dispute, but as a stakeholder in a failing regional security model. The U.S. objective is to secure a commitment from Beijing to diversify its energy imports toward U.S. Liquefied Natural Gas (LNG), thereby reducing the U.S. trade deficit while simultaneously decoupling China from the IRGC’s financial networks.

The Semiconductor Sovereignty Gap

The primary subtext of the May visit is the "Entity List" and the restricted flow of advanced lithography equipment. China’s "Made in China 2025" initiative has hit a hardware ceiling. While Chinese firms have made strides in software and AI application, they remain 3-5 generations behind in the fabrication of sub-7nm chips.

The U.S. strategy involves a "Tiered Access" negotiation model. Instead of a binary ban, the administration is moving toward a performance-threshold system.

- Tier 1 (Unrestricted): Legacy nodes (28nm and above) for consumer electronics and automotive sectors.

- Tier 2 (Conditional): 14nm to 10nm nodes, subject to end-user verification to ensure no military dual-use.

- Tier 3 (Prohibited): Extreme Ultraviolet (EUV) lithography and AI-accelerated chips capable of processing large-scale surveillance data.

By holding the summit in mid-May, the U.S. allows for the publication of Q1 earnings from major Silicon Valley firms. These reports will quantify the "China Revenue Leakage." If U.S. firms show resilience despite the export bans, Trump enters the Beijing meeting with a "Maximum Pressure" mandate. If the earnings show catastrophic losses, Xi gains the leverage to demand a total removal of the Entity List in exchange for agricultural purchase quotas.

The Currency Valuation Equilibrium

The valuation of the Renminbi (RMB) against the USD remains the most volatile variable in the bilateral relationship. The "7.0 Threshold" is the psychological and economic barrier that dictates trade flows. When the RMB weakens beyond this point, Chinese exports become cheaper, effectively neutralizing U.S. tariffs.

A core component of the May 14 agenda is the "Currency Transparency Protocol." The U.S. Treasury seeks a binding agreement that prevents "Competitive Devaluation." The mechanics of this protocol include:

- Direct Intervention Reporting: Requirement for the People’s Bank of China (PBOC) to disclose its activities in the offshore RMB market within 24 hours.

- Interest Rate Symmetry: A soft alignment of interest rate cycles to prevent massive capital flight from China, which would naturally depress the currency.

- Reserve Composition: A commitment to maintaining a specific ratio of USD-denominated assets to ensure China remains incentivized to support the strength of the dollar.

The risk for the U.S. is "Policy Overhang." If the demands are too stringent, the PBOC may opt for a "Managed Float" that leads to a sharp, one-time devaluation, triggering a global deflationary shock. The May 14 summit is designed to prevent this "Nuclear Option" by offering a phased reduction in Section 301 tariffs in direct proportion to RMB stability.

Structural Bottlenecks in the "Phase Two" Agreement

Most analysts focus on the "Phase One" purchase agreements—the billions of dollars in soybeans and Boeing aircraft. However, the May summit is the opening salvo for "Phase Two," which targets the structural core of the Chinese economic model.

The State-Owned Enterprise (SOE) Subsidy Problem

The U.S. demands a dismantling of the "Big Fund" and other state-led investment vehicles that provide interest-free capital to Chinese tech giants. From the Chinese perspective, this is a matter of national survival. From the U.S. perspective, it is a matter of market fairness. The May 14 talks will likely attempt to define "Neutrality Zones"—sectors where SOEs are allowed to operate without U.S. interference (e.g., domestic infrastructure) versus sectors where they must face anti-subsidy duties (e.g., 5G, Green Energy).

Intellectual Property (IP) Theft and Forced Tech Transfer

The legal framework for IP protection in China has improved on paper, but enforcement remains localized and inconsistent. The U.S. is pushing for a "Reversed Burden of Proof" in trade secret litigation. This means if a Chinese company produces a product substantially similar to a U.S. patent-holder’s design within a short window of a joint venture, the Chinese company must prove they developed it independently.

The Geopolitical Risk of the "May Window"

The timing of the May 14-15 visit is not accidental. It occurs just prior to the typhoon season in the South China Sea and after the conclusion of the "Two Sessions" political meetings in Beijing. This ensures that President Xi has his domestic mandate solidified before meeting Trump.

However, several "Black Swan" events could derail the summit:

- The Taiwan Strait Friction: Any significant arms sale or high-level diplomatic transit between Washington and Taipei in April would likely result in a second cancellation of the May visit.

- The Iranian Retaliation Cycle: If Tehran follows through on threats to close the Strait of Hormuz in response to U.S. pressure, the resulting oil spike (projected at $110+ per barrel) would shift the summit's focus from trade to emergency energy rationing.

- The U.S. Election Cycle: As the American primary season intensifies, the political cost of a "Soft Deal" increases for Trump. He cannot afford a compromise that looks like a retreat, which may force him into an "All-or-Nothing" stance that Beijing cannot accept.

Strategic Forecast and Recommendation

The May 14-15 summit will not result in a comprehensive treaty. The interests are too divergent and the mistrust too deep. Instead, the outcome will be a "Managed Competition Protocol."

Expect the following tactical shifts:

- The Agriculture-for-Chips Swap: China will commit to a three-year, $50 billion annual purchase of U.S. agricultural products in exchange for "License Exceptions" for non-military semiconductor components.

- The Maritime De-escalation Zone: A verbal agreement to reduce the frequency of "Freedom of Navigation" operations in exchange for a freeze on further militarization of artificial islands in the South China Sea.

- The Digital Yuan Carve-out: The U.S. will likely allow the continued development of China’s Central Bank Digital Currency (CBDC) as long as it is not used to bypass the SWIFT banking system for sanctioned entities.

Organizations with exposure to the trans-Pacific supply chain should not view the May 14 summit as a signal to return to "Business as Usual." The underlying trend is "High-Friction Decoupling." Companies should continue to diversify manufacturing bases into Vietnam, India, or Mexico (the "China Plus One" strategy) regardless of the summit's public-facing rhetoric. The May meetings are a volatility-dampening exercise, not a resolution of the systemic rivalry between the world’s two largest economies. The window for zero-tariff trade has closed permanently; the goal now is simply to manage the rate of escalation.